What are scope 1, 2 and 3 carbon emissions?

Many organisations are seeking to reduce their greenhouse gas emissions. When it comes to reporting progress, you’ll often see the terminology ‘Scopes 1, 2 and 3 emissions’ used, but what do these numbers actually mean?

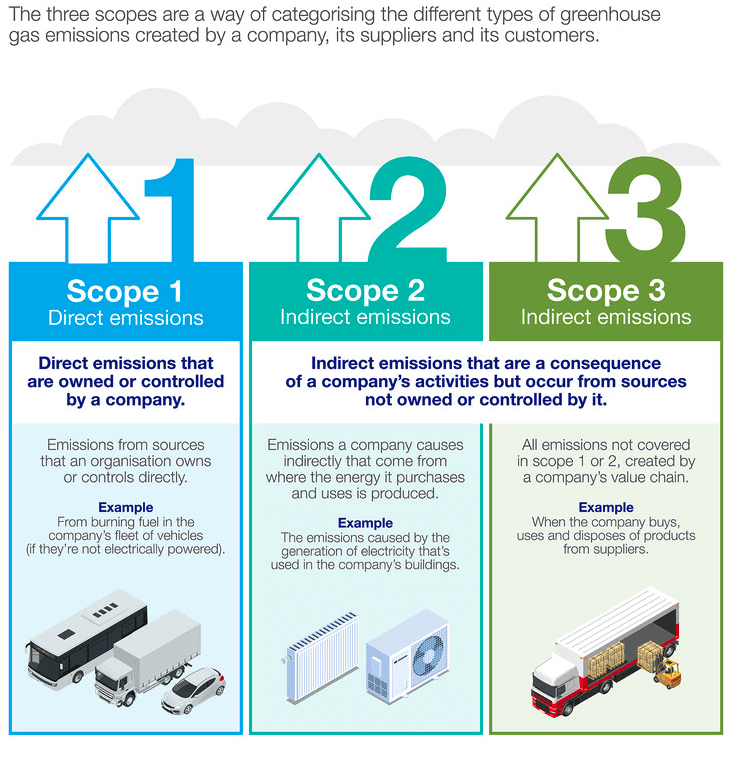

On the road to net zero, one of the main ways that companies’ greenhouse gas emissions are measured and assessed is to look at them within three different ‘scopes’.

Why are there three scopes of emissions?

In order to take action to reduce emissions, we need to understand and measure where they’re sourced from in the first place.

The three scopes are a way of categorising the different kinds of emissions a company creates in its own operations and in its wider ‘value chain’ (its suppliers and customers).

It’s not clear why they’re called ‘scopes’ rather than ‘groups’ or ‘types’ but the name comes from the Greenhouse Gas Protocol, which is the world’s most widely used greenhouse gas accounting standard.

As the Greenhouse Gas Protocol itself puts it: “Developing a full [greenhouse gas] emissions inventory – incorporating Scope 1, Scope 2 and Scope 3 emissions – enables companies to understand their full value chain emissions and focus their efforts on the greatest reduction opportunities”.

Definitions of scope 1, 2 and 3 emissions

Essentially, scope 1 are those direct emissions that are owned or controlled by an organisation, whereas scope 2 and 3 indirect emissions are a consequence of the activities of the company but occur from sources not owned or controlled by it.

Scope 1 emissions

Scope 1 covers emissions from sources that an organisation owns or controls directly – for example from burning fuel in our fleet of vehicles (if they’re not electrically-powered).

Scope 2 emissions

Scope 2 are emissions that a company causes indirectly and come from where the energy it purchases and uses is produced. For example, the emissions caused when generating the electricity that we use in our buildings would fall into this category.

Scope 3 emissions

Scope 3 encompasses emissions that are not produced by the company itself and are not the result of activities from assets owned or controlled by them, but by those that it’s indirectly responsible for up and down its value chain. An example of this is when we buy, use and dispose of products from suppliers. Scope 3 emissions include all sources not within the scope 1 and 2 boundaries.

Original Source: National Grid